look news india

look news india

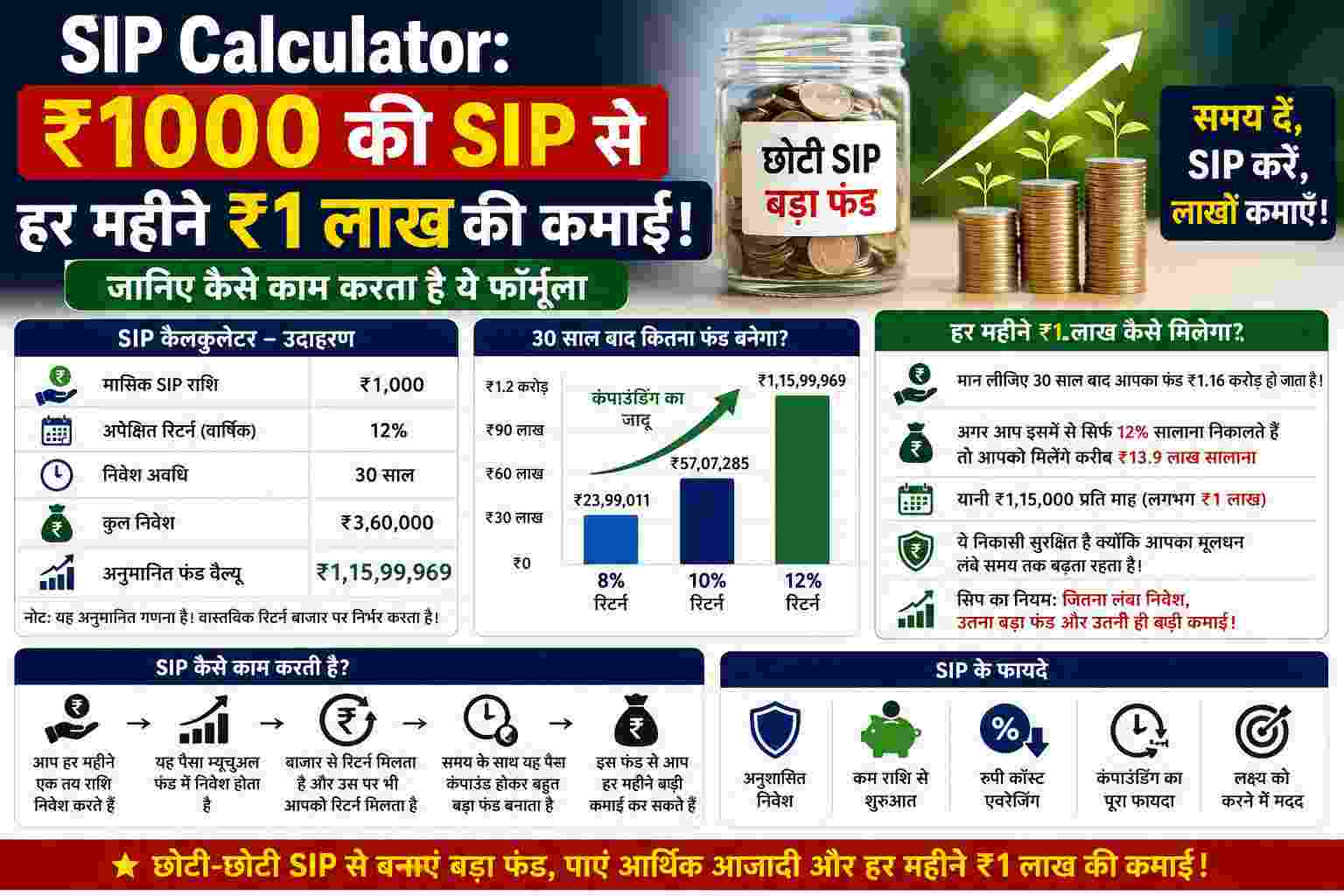

Step-up SIP and SWP Calculator: Every person wants that his regular income does not stop after retirement and he can live his life with self-respect. The good thing is that your initial salary does not have to be huge to create a big corpus in old age. If you start a small Systematic Investment Plan (SIP) at an early age, step-up it every year, and continue investing with patience for a long time, then with the magical power of compounding, you can create a fund worth crores by retirement.

After this, by shifting the same deposited capital to Systematic Withdrawal Plan (SWP), a huge amount can be obtained every month like a fixed salary or pension. Let us understand the complete mathematics of building a fund of ₹1.05 crore from a humble beginning of ₹1,000 and then getting ₹1 lakh every month.

How to build a corpus of ₹1.05 crore from a SIP of ₹1,000? (mathematics of compounding)

Suppose your age is currently 28 years And you have decided to start investing. You start a SIP of just ₹1,000 every month. As your annual salary or increment in job increases, you also increase your SIP by 10% step-up every year (for example: ₹ 1000 per month in the first year, ₹ 1100 per month in the second year, ₹ 1210 per month in the third year, etc.).

If you continue investing with this discipline till 60 years of your age (retirement) i.e. for full 32 years and you get average returns from mutual funds. 12% annual return If you get it, the complete outline of your investment will look like this:

-

Total investment period: 32 years (from age 28 to age 60)

-

Initial Monthly Investment: ₹1,000 (with 10% annual step-up)

-

Total investment out of your pocket: ₹24.13 lakh

-

Total profit from compounding: ₹80.98 lakh

-

Estimated fund ready at 60 years: ₹1.05 crore

Why is Step-Up a gamechanger?

If you had continued to do SIP of only ₹ 1,000 per month without increasing the amount for the entire 32 years, it would have been almost impossible to reach the magical figure of ₹ 1 crore. This small increase of just 10% in investment every year makes a huge difference of crores of rupees in the long run.

How to get ₹1 lakh every month after retirement? (SWP’s formula)

When you have a big corpus ready at retirement (at the age of 60), you do not need to spend or lose tax by withdrawing the entire money in a bank account at once. This is where it comes in handy Systematic Withdrawal Plan (SWP)which is a tool of mutual fund where your money remains invested in the market and earns returns and you also get a fixed amount of your choice every month.

Now suppose, with the help of various investments and asset allocation, you have Total fund of ₹1.5 crore It is deposited. For safety, you transfer this entire fund to a debt mutual fund or conservative hybrid fund.

If you have to spend only annually on this secure fund Fixed return of 6% Keep getting it and you every month Withdrawal of ₹1 Lakh (SWP) If we set it, its mathematics will be something like this:

-

Initial Total Investment (in SWP): ₹1.5 crore

-

Pension received every month: ₹1 lakh

-

Pension/Withdrawal Period: 12 years

-

Total deposit withdrawal in 12 years: ₹1.44 crore

-

Estimated earnings earned by the fund during withdrawal: ₹43.13 lakh

The biggest advantage of this strategy is that you will continue to get regular income of ₹ 1 lakh every month and your original capital (₹ 1.5 crore) will also remain safe in the market and earn additional returns, due to which your fund will never go to zero suddenly.

Always remember 3 important things before starting your investment journey

-

Uncertainty of Retirement and Returns: The return of 12% in mutual funds or 6% in debt funds is completely estimated, it is not guaranteed like a fixed deposit (FD). Depending on market fluctuations, this return may be more or less in the long term.

-

Periodic Review (Portfolio Review): As you approach your retirement (60 years) (at around 55 years of age), start withdrawing money from your high-risk equity funds and gradually shift to safer debt options so that your funds are not affected by a market crash.

-

Don’t forget inflation: The purchasing power (value) of ₹ 1 lakh today will not be the same 30 or 32 years from now due to inflation. So as your income increases, try increasing your SIP step-up rate from 10% to 15% so that your fund can easily beat inflation.