look news india

look news india

Choosing the right investment vehicle is the most important step for major future financial goals—like children’s higher education, marriage, owning a home or building a retirement fund. When it comes to long-term secure and bumper wealth creation, Public Provident Fund (PPF) and Systematic Investment Plan (SIP) in mutual funds are among the most popular and trusted options among Indian investors.

Often there is a dilemma in the minds of investors as to which of these two options is better in terms of making money. Investment decision should not be taken only on the basis of returns but also on the basis of risk appetite and tax planning. Let us understand through mathematics that if a person invests ₹ 5,000 every month for 30 years, then how much money will be generated on maturity in both the options.

1. 30 years math in PPF: Guaranteed fund with government security

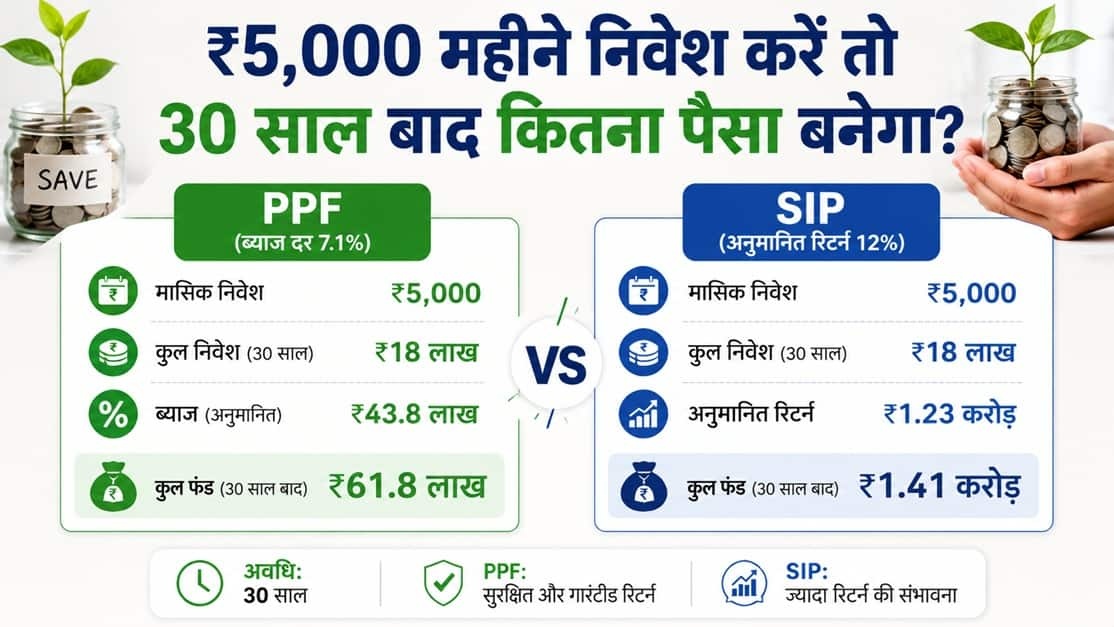

Public Provident Fund (PPF) is best for those who want a completely safe investment away from market fluctuations. currently on ppf Annual interest rate of 7.1% is being received (which is reviewed by the Central Government every quarter).

If this interest rate remains constant for 30 years and you deposit ₹5,000 every month, your fund will grow like this:

-

Your Total Investment (Principal): ₹18,000,000 (in 30 years)

-

Estimated Interest Earned: Approximately ₹43,80,000

-

Total Fund on Maturity: Approximately ₹61,80,000

Note: The basic lock-in period of PPF is 15 years, but after maturity, you can extend it in blocks of five years each. In a journey of 30 years, your total fund will be ₹ 61.80 lakh, with double the amount invested only through compounding interest.

2. 30 years of mathematics in SIP: You will become a millionaire with the power of compounding.

Systematic Investment Plan (SIP) is a means of investing in the equity market through mutual funds. If we look at the long term (30 years) history, equity mutual funds have on an average 12% annual return Delivered easily.

If you continue SIP of ₹5,000 every month for 30 years, the wealth gains will be as follows:

-

Your Total Investment (Principal): ₹18,000,000 (in 30 years)

-

Estimated Wealth Gain (Returns): Approximately ₹1,23,000,000

-

Total Fund at Maturity (Estimated Wealth): More than about ₹1.41 crore

The difference is clear: While PPF will fetch you up to ₹61.80 lakh, your same monthly investment of ₹5,000 can create a huge corpus of ₹1.41 crore thanks to compounding in SIP. However, keep in mind that SIP returns are completely subject to market risks and there is no fixed guarantee.

The bitter truth about inflation

Financial advisors always caution that the inflation rate should never be ignored while calculating investments. The purchasing power of today’s ₹1 crore will be greatly reduced after 30 years.

-

Estimating Actual Value: If we assume 12% annual return on SIP and the country’s average inflation rate of 6%, then after 30 years the real value of your fund of ₹ 1.41 crore will be equal to today’s ₹ 40.84 lakh. This would include your original investment of ₹18 lakh and actual returns of ₹22.84 lakh. Therefore, future goals should always be planned taking inflation into account.

Comparison Chart: SIP vs PPF

| Features/Factors | Systematic Investment Plan (SIP) | Public Provident Fund (PPF) |

| estimated rate of return | 12% to 15% (market based, estimated) | 7.1% (government, fixed but variable) |

| Total fund after 30 years | Approximately ₹1.41 crore | Approximately ₹61.80 lakh |

| amount of risk | Medium to high (depending on market fluctuations) | Zero (100% sovereign guarantee of the Central Government) |

| Tax benefits | Long Term Capital Gains (LTCG) tax payable on returns | EEE category (Investment, interest and maturity all tax-free) |

| Liquidity (clearance) | Can be closed or partially removed at any time | Lock-in of 15 years (partial withdrawal possible after 5 years) |

| loan facility | not available | Available (loan possible up to 25% of deposit after 1 year) |

Both investment vehicles have their own special characteristics

Why do investors prefer SIP?

-

Rupee Cost Averaging: You get more units when the market is down and less when it is up, which balances your purchase cost in the long run.

-

Flexibility: You can start with just ₹500 and stop or increase it at any time if needed.

-

Features of SWP: At the time of retirement you Systematic Withdrawal Plan (SWP) Through this, you can get a fixed amount like pension every month from this fund, due to which the entire investment does not get lost all at once.

Why investors choose PPF?

-

Zero Risk and Tax Savings: In the old tax regime, exemption up to ₹1.5 lakh is available under Section 80C and the entire interest received is completely tax-free.

-

Financial Discipline: Due to the strict lock-in period of 15 years, this money remains safe and is not wasted in unnecessary expenditure.

Final Conclusion: Which option is best for you?

If you are in the early stages of your career, you are young, you can take risks and your primary goal “Making more and more wealth” yes, then for you SIP An excellent and attractive option. On the contrary, if you are nearing retirement or do not want any kind of risk on your hard-earned money and “Capital protection and tax exemption” If your priority is ppf Most suitable for you.

Smart Financial Advice: Most financial planners recommend a hybrid model under asset allocation. You can split your ₹5,000 budget—say do a SIP of ₹3,500 and put ₹1,500 in PPF. This will give you the unmatched security and tax benefits of PPF, and will also provide you with high market returns and the opportunity to become a millionaire through SIP.